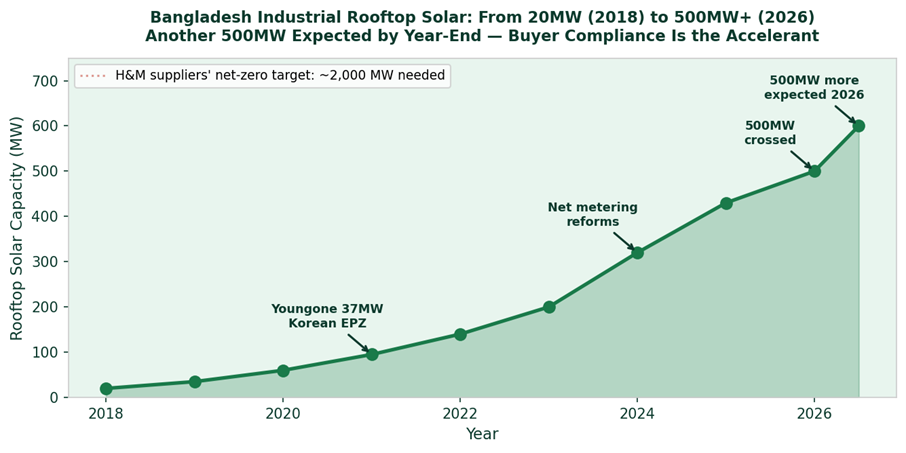

Bangladesh’s industrial rooftop solar sector has crossed a milestone that would have been inconceivable five years ago: more than 500 megawatts of capacity installed across factories nationwide. Solar developers report that another 500 megawatts is expected to be commissioned before the end of 2026, driven by a combination of buyer compliance requirements, falling equipment costs, and — most immediately — the energy security shock caused by the Middle East conflict’s disruption of LNG supply chains.

Bangladesh industrial rooftop solar growth 2018–2026: from 20MW to 500MW+ – the acceleration driven by buyer compliance requirements, with another 500MW pipeline for 2026

The economics have shifted decisively. Installing one megawatt of rooftop solar capacity now costs approximately Tk 3.5 crore — down from Tk 5.5 crore two years ago, according to Masudur Rahim of Omera Solar. At current grid electricity tariff rates and with load-shedding adding diesel generator costs, rooftop solar typically pays back in four to six years. The Middle East war, which drove up fuel prices and created the diesel rationing crisis that disrupted production in April 2026, compressed that payback calculation further for every factory that experienced production shutdowns.

H&M’s suppliers alone would need around 2,000MW of renewable energy to achieve net-zero. Total installed industrial rooftop solar in Bangladesh: 500MW. The compliance gap is four times what has been built.

The buyer compliance angle is the structural driver. Masudur Rahim was direct: ‘Many global brands now encourage or require their suppliers to adopt renewable energy.’ American Eagle demands that at least 10% of electricity used by tier-one and tier-two suppliers come from renewables now, not by 2030. Levi Strauss and GAP have pledged 42% supply chain emissions cuts by 2030. Factories nominated by H&M alone would require around 2,000 MW of renewable energy for net-zero against the 500 MW currently installed across the entire industrial sector.

The leading installations demonstrate what is achievable. Youngone Corporation in Chattogram’s Korean Export Processing Zone built 37 MW across its complex — Bangladesh’s largest rooftop solar installation, producing 120 to 140 megawatt-hours daily. Ha-Meem Group’s 12.2 MW system has cut facility emissions by approximately 6% and is expanding. Scube has delivered 254.9 MW across 210 projects with 90 more MW in the pipeline. Solaric has implemented 162 MW with 60–80 MW expected this year.

The structural barrier remains financing access for smaller factories. IDCOL has financed rooftop solar in over 150 factories, but scaling beyond the large-cap manufacturers requires bank lending products designed for solar — with longer tenors, lower rates, and asset-backed structures that reflect solar’s revenue-generating nature rather than treating it as standard capital expenditure. The Bangladesh Energy Regulatory Commission’s 2025 net-metering reforms, which allow factories to export surplus electricity to the grid for credits, improve the investment case further.

Bangladesh reached 500 MW through market forces and buyer requirements — without a dedicated government incentive programme for industrial solar. The next 500 MW faces the same pathway. But the 2,000 MW that H&M’s suppliers alone would need for net-zero compliance will require policy intervention: dedicated financing facilities, removal of the 58.6% import duty on solar equipment for export-oriented manufacturers, and a grid wheeling framework that makes large-scale off-site solar procurement viable.