Two reports published within weeks of each other in early 2026 frame Bangladesh’s climate-economic dilemma with unusual precision. Taken together, they describe not just an environmental challenge but a macroeconomic choice with consequences that compound over the next three decades.

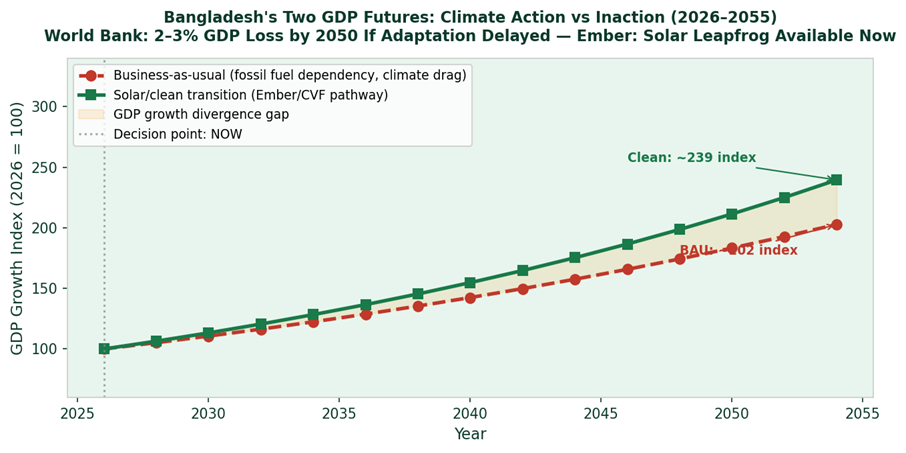

Two GDP trajectories for Bangladesh 2026–2055: business-as-usual fossil fuel dependency (World Bank: 2–3% growth drag by 2050) vs clean energy leapfrog path (Ember/CVF), the divergence compounds over time

The first, a March 2026 analysis published in The Business Standard drawing on World Bank research, quantifies the cost of climate inaction for Bangladesh. Multiple World Bank studies suggest that if adequate adaptation measures are not taken now, Bangladesh’s GDP growth rate could fall by 2 to 3 percentage points by 2050. The mechanisms are specific and already visible: rising sea levels increasing coastal salinity and destroying agricultural land in the southwest; more frequent and severe flooding disrupting production and infrastructure; extreme heat reducing worker productivity across manufacturing, construction, and agriculture; and the accelerating migration from coastal areas to already-overcrowded cities, straining every urban system from water supply to healthcare.

The second report, published in early April 2026, presents a different frame. The Ember analysis, conducted alongside the Climate Vulnerable Forum and V20 Finance Ministers, argues that Bangladesh and similar emerging economies are not locked into the traditional fossil fuel development pathway. The ‘Electric Fast-Track for Emerging Markets’ report finds that solar power, battery storage, and electrification now offer Bangladesh a viable path to leapfrog directly from energy scarcity to energy abundance — at lower cost, faster deployment speed, and with dramatically reduced import dependence.

65% of Bangladesh’s electricity generation depends on imported fuel. Every percentage point shifted to domestic solar reduces exposure to the geopolitical shocks that disrupted production in April 2026.

The numbers that connect these two reports are striking. Bangladesh currently imports approximately 65% of its commercial energy — primarily LNG and refined petroleum products, primarily from the Middle East, through logistics chains that the ongoing regional conflict has already demonstrated can be disrupted at speed. IEEFA’s Shafiqul Alam noted that the April 2026 energy crisis exposed exactly this vulnerability: ‘In the last decade and a half, Bangladesh ramped up power generation capacity mostly relying on fossil fuels, which has exposed the country to volatile international energy prices.’

The Ember analysis finds that solar is now less capital-intensive than fossil fuel power, that solar-plus-battery systems can deliver electricity independently of grid expansion, and that decentralised renewable energy deployment is already more cost-effective than extending the national grid in many cases. Bangladesh’s industrial rooftop solar boom — crossing 500 MW in 2026 — is proof of concept for this pathway at factory scale. The question is whether national energy and economic policy reflects the same logic.

Climate resilience and economic growth are not competing priorities for Bangladesh. They are the same priority. Every year of delayed renewable transition adds to the cumulative climate adaptation cost. Every year of continued fossil fuel import dependence amplifies the geopolitical risk exposure that disrupted industrial production in April 2026. Bangladesh’s budget, its financial sector’s capital allocation, and its trade negotiation positions need to treat this not as an environmental question but as the macroeconomic planning question it has become.