Bangladesh’s garment sector has navigated currency shocks, pandemic shutdowns, and a decade of intensifying regulatory pressure. April 2026 was different. Three simultaneous crises arrived from three separate directions, creating a convergence that exposed the sector’s structural vulnerabilities in real time.

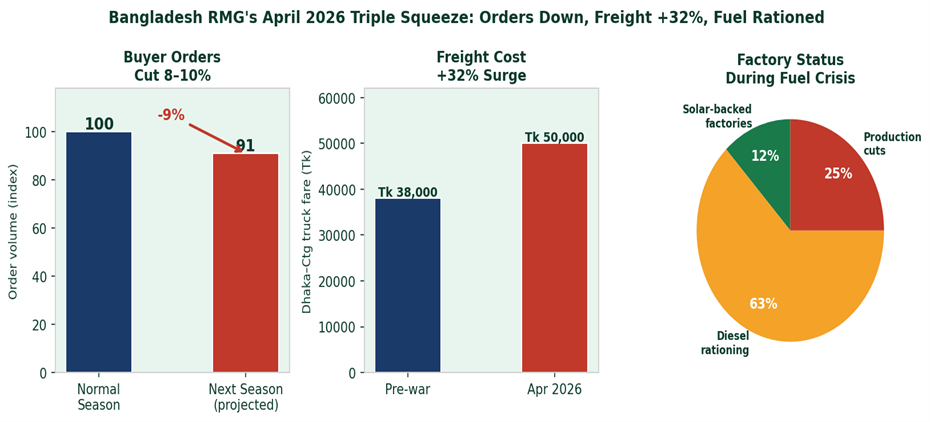

The first shock was commercial. A senior official at a leading European buying house confirmed that 8–10% of garment work orders will be cut for the next season. European retailers are managing large volumes of unsold winter inventory, compressing their forward buying. In a sector where volume directly determines factory utilisation and worker income, this is not a minor adjustment — it is a significant contraction.

April 2026 triple squeeze: buyer orders down 8–10%, Dhaka–Chattagram freight +32%, and factory production status during diesel rationing — only solar-backed factories maintained full output

The second shock was energy. The Middle East conflict disrupted global LNG supply chains and drove fuel prices sharply higher across South Asia. Bangladesh, which imports over 57% of commercial energy and depends heavily on gas-fired generation, felt the impact immediately. Since April 13, BGMEA has operated a diesel priority card system for member factories. Despite this, overall factory productivity declined due to insufficient fuel availability.

The April 2026 energy crisis was a live field test of ESG investment. Factories with solar passed. Factories without it failed. On-time delivery records will tell the story.

The third shock was logistical. Truck fares between Dhaka and Chattagram rose from Tk 38,000 to Tk 50,000 — a 32% surge — following the war-driven fuel price spike. This arterial route carries virtually every export shipment Bangladesh makes. A 32% freight cost increase on every outbound container adds directly and unavoidably to cost structures across the entire sector.

The ESG dimension of this crisis was immediate and visible. Factories with rooftop solar backup — like Ha-Meem Group’s 12 MW installation — continued operating at full capacity through the diesel rationing period. Those dependent entirely on grid power or diesel generators faced production cuts, delayed shipments, and in some cases temporary shutdowns. The on-time delivery records for April 2026 will reflect this difference. Buyers tracking supplier reliability will allocate future orders accordingly.

April 2026 is the month the business case for renewable energy became an operational fact rather than a theoretical projection. Energy resilience is supply chain resilience. Factories that made that investment are demonstrating it now. The factories that deferred it because margins were tight are learning that the cost of deferral is higher than the cost of investment. ESG is not a reporting exercise. It is an operational framework. April 2026 proved it.