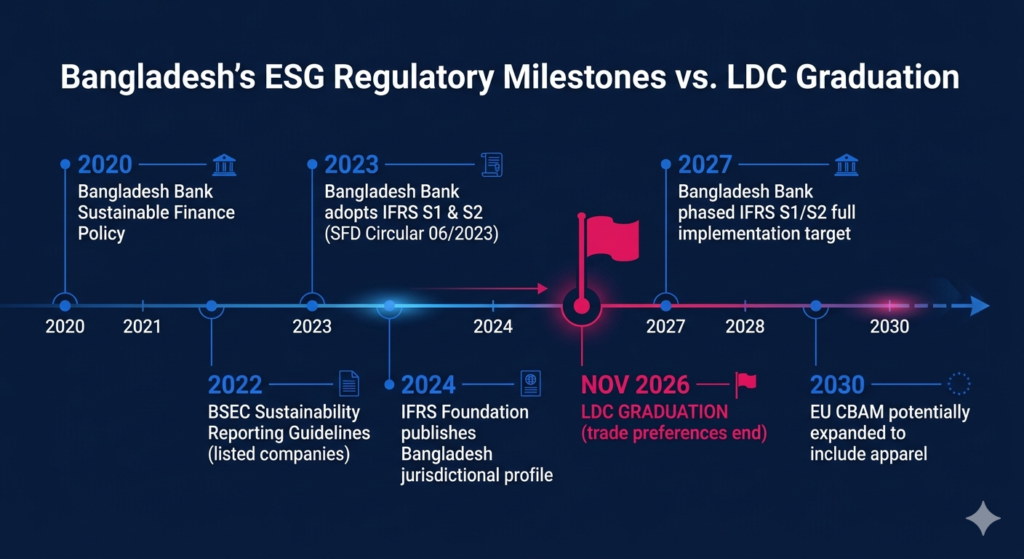

On 24 November 2026, Bangladesh officially graduates from the United Nations’ list of Least Developed Countries.

In diplomatic language, this is a milestone. A recognition of progress. Decades of growth in garments, remittances, and development indicators finally acknowledged on the world stage. It sounds like something to celebrate — and in some ways, it is.

But in the language of global trade and investment, LDC graduation is also a cliff edge.

It means losing duty-free, quota-free access to the EU — preferences that have underwritten our garment export model for decades. It means losing eligibility for concessional finance from multilateral institutions. It means entering a more competitive global market as a “developing economy” competing against countries that had decades more time to build competitiveness infrastructure.

The question is not whether Bangladesh can survive graduation. We can, and we will. The question is: what gives us the right to continued investor confidence, buyer loyalty, and market access once the preferential scaffolding comes down?

The answer, increasingly, is ESG.

What Investors Are Actually Asking Now

Global ESG assets under management are expected to surpass $40 trillion by 2030. The investors allocating that capital are not looking for countries with the lowest wages. They are looking for countries with credible sustainability frameworks, transparent governance, and measurable environmental performance.

Bangladesh’s pitch to that investor community, post-LDC, cannot be “we are cheap.” That pitch has a shelf life. The pitch must be: “We are compliant, transparent, and improving — here is the data.”

Right now, we cannot make that pitch. Not credibly. Only 16 Bangladeshi companies are in the Bloomberg ESG universe. BSEC has made sustainability reporting mandatory for listed companies, but even among those companies, most ESG reports read like marketing brochures rather than accountability documents. Bangladesh Bank has adopted IFRS S1 and S2 for banks, but awareness among bank management remains critically low.

The gap between regulation on paper and practice on the ground is wide. And it is closing — but not fast enough.

| Country | Companies in Bloomberg ESG Universe | Mandatory ESG Reporting | ISSB Adoption Status |

|---|---|---|---|

| India | 400+ | Yes (top 1,000 listed) | In progress |

| Pakistan | 50+ | Partial | Adopting |

| Sri Lanka | 30+ | Voluntary | Partial |

| Bangladesh | 16 | Listed companies only | Banks (IFRS S1/S2) |

| Vietnam | 40+ | Voluntary | Developing |

Sources: Bloomberg ESG data; IFRS Foundation jurisdictional profiles; TBS News, 2026

Why This Is Also an Opportunity

It is worth pausing on the other side of this argument, because doom narratives are easy and incomplete.

Bangladesh’s LDC graduation coincides with a moment when ESG frameworks are being adopted across Asia at remarkable speed. The IFRS Foundation has published jurisdictional profiles for 17 countries committing to ISSB standards — Bangladesh is among them. China’s listed companies must publish ESG reports by April 30, 2026. Japan’s Tokyo Prime Market firms face mandatory climate disclosure from 2027. The direction of travel in Asia is clear, and Bangladesh, for once, has a regulatory head start through Bangladesh Bank’s IFRS S1/S2 adoption.

The question is execution. And execution requires people who know how to do it.

The Professional Who Does Not Exist Yet

Walk into most Bangladeshi companies today — banks, pharma, FMCG, telecom — and ask who owns sustainability reporting. You will either get a confused look, a junior CSR officer whose job is to write the annual report paragraph about tree planting, or a CFO who has heard of GRI but never filed a disclosure under it.

The sustainability professional that post-LDC Bangladesh needs — someone who can measure carbon emissions, prepare GRI-aligned reports, understand IFRS S2 climate disclosures, and advise on ESG strategy — barely exists at scale in this country.

This is not a criticism. It is a market gap. Every market gap is a story about supply catching up to demand. The demand is here. LDC graduation is the forcing function. What remains is building the supply of professionals who can meet it.

The Window Is Narrower Than You Think

There is a temptation to treat November 2026 as a distant event. It is not. Trade preference changes have lead times. Buyer decisions about sourcing are made 12 to 18 months in advance. Investor due diligence on ESG credentials takes time. The companies and professionals that begin building ESG capability now will be positioned when the gate changes. Those who wait for the gate to close will find the queue very long.

Bangladesh has a narrow but real window to turn LDC graduation from a vulnerability into a relaunch. But that window requires action now — from companies, from professionals, from institutions.

ESG Institute Bangladesh is Bangladesh’s only dedicated ESG education and advisory institute. We offer professional certification, corporate training, and sustainability reporting advisory built specifically for the Bangladesh context. The ESG Excellence Awards Bangladesh 2026 recognise organisations already building this future. Applications open now.

Professional Trainings (Diploma, Accreditations, In-Depth Workshops): https://esginstitutebd.com/ | Join the 2026 ESG Awards: esgawardsbd.com