There is a data point buried in a recent Business Standard analysis of ESG and Bangladesh’s capital market that deserves far more attention than it received: only 16 Bangladeshi companies are currently included in the Bloomberg ESG universe.

Sixteen.

Out of more than 350 companies listed on the Dhaka Stock Exchange. In a country of 170 million people with one of the fastest-growing economies in Asia for the past two decades. With a garment sector that supplies H&M, Zara, and Walmart. With a pharmaceutical industry that exports to 150 countries. With a banking sector that has adopted IFRS S1 and S2 ahead of most of its South Asian peers.

Sixteen companies that a global ESG-oriented investor can actually see in their data system.

This is not a technical problem. It is a disclosure problem. And a disclosure problem is a knowledge problem.

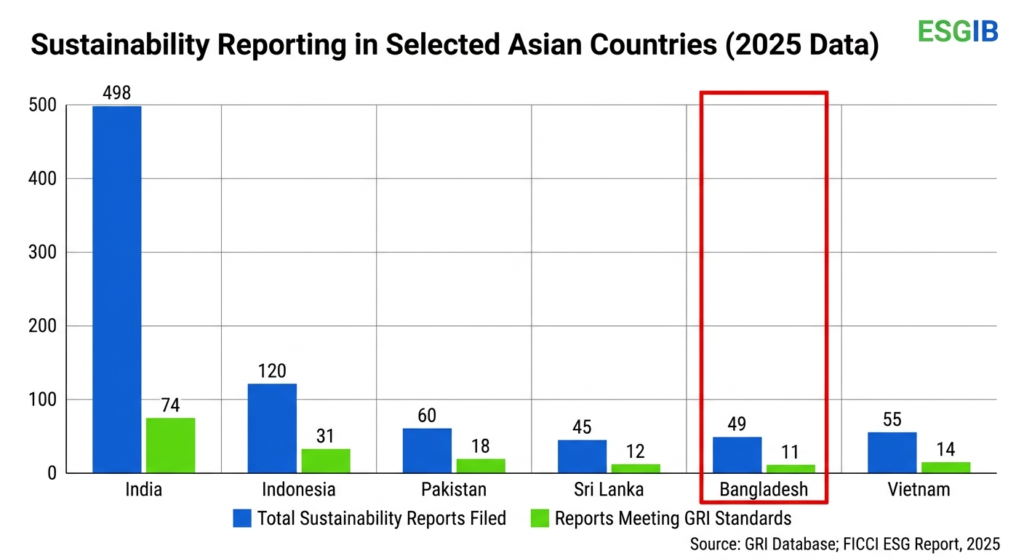

Chart: GRI Sustainability Reports Filed — Bangladesh vs. Peers (2020 Data, GRI Database)

Why ESG Visibility Is Not Optional for Capital Markets

Here is how global investment actually works in 2026. A fund manager at a sustainable investment firm in Amsterdam is allocating capital across emerging markets. She opens Bloomberg. She filters by ESG score. Bangladesh essentially does not appear — not because Bangladeshi companies are poorly governed or environmentally irresponsible, but because they have never told anyone.

The companies that do appear in her screen include Grameenphone, BAT Bangladesh, BRAC Bank, Square Pharmaceuticals, Walton Hi-Tech, and a handful of others. These are good companies. But they represent a tiny fraction of the market, and their inclusion says more about their parent company relationships with international reporting norms than about any deliberate national ESG strategy.

The rest of the market is invisible to global capital — and invisible assets do not attract investment.

Meanwhile, Bangladesh’s capital market has struggled with investor confidence since the crash of 2010. Frequent policy changes, governance concerns, and lack of transparency are consistently cited as the reasons foreign portfolio investment remains modest. ESG reporting — properly done — addresses all three of these directly. It creates a structured, internationally comparable record of how a company is governed, how it manages risk, and how it treats its workers and environment.

The Regulatory Framework Is Already There

What is striking about Bangladesh’s ESG disclosure situation is that the regulatory architecture is not absent — it is just unenforced and under-resourced.

The Bangladesh Securities and Exchange Commission has made ESG reporting mandatory for listed companies under its Sustainability Reporting Guidelines. Bangladesh Bank has adopted IFRS S1 and S2 through its 2023 circular, creating a framework for climate and sustainability disclosure across banks and financial institutions. The Dhaka Stock Exchange is working with GRI to enable listed companies to prepare sustainability reports.

The rules exist. The problem is implementation. Most listed companies either do not know how to prepare a credible sustainability report, do not have the internal capacity to do so, or treat the requirement as a box-ticking exercise that generates documents nobody reads.

BSEC’s own spokesperson has acknowledged that the current Corporate Governance Code only partially covers ESG standards, and revision work is underway. But regulatory revision moves slowly. Market competitiveness does not wait.

What a Credible ESG Report Actually Requires

A sustainability report that gets a company into the Bloomberg ESG universe — or onto the radar of any serious ESG-oriented investor — is not a CSR annual report with photographs of tree-planting events.

It requires:

- Quantified environmental data: energy consumption, water use, waste generated, Scope 1 and 2 greenhouse gas emissions

- Social metrics: worker safety rates, gender diversity, fair wage disclosures, supply chain labour standards

- Governance disclosures: board composition, anti-corruption policies, executive remuneration linked to sustainability targets

- A recognised framework: GRI, IFRS S1/S2, or SASB — consistently applied year on year

- Assurance: ideally third-party verification of the data

Very few Bangladeshi companies currently meet more than two of these five criteria. The gap is not regulatory — it is professional capacity. Companies need people who know how to collect this data, structure it under a recognised framework, and present it in a way that builds rather than destroys credibility.

The Business Case for Getting This Right

The argument for ESG disclosure is not idealistic. It is financial.

Companies with credible ESG reporting attract a wider investor base. They access better borrowing terms through ESG-linked loans and green bonds. They retain international buyers who increasingly require ESG data from suppliers. They reduce regulatory risk as disclosure requirements tighten. And in Bangladesh’s specific context, they position themselves for the post-LDC investment environment where trade preferences are gone and governance credibility becomes the competitive differentiator.

The 16 companies already in the Bloomberg ESG universe are not there by accident. They invested in disclosure. The question for the other 334 is how long they can afford not to.

ESG Institute Bangladesh is Bangladesh’s only dedicated ESG education and advisory institute. We offer professional certification, corporate training, and sustainability reporting advisory built specifically for the Bangladesh context. The ESG Excellence Awards Bangladesh 2026 recognise organisations already building this future. Applications open now.

Professional Trainings (Diploma, Accreditations, In-Depth Workshops): https://esginstitutebd.com/| Join the 2026 ESG Awards: esgawardsbd.com