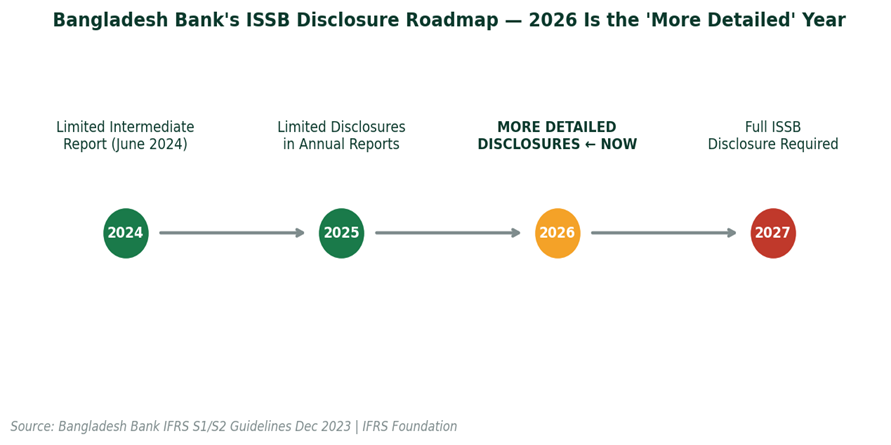

Bangladesh Bank ISSB disclosure roadmap 2024–2027 — 2026 is the “more detailed disclosures” year, currently active. Banks that miss this phase risk being excluded from international green capital markets

In June 2025, the IFRS Foundation published its first set of formal jurisdictional profiles, a public record of which countries have achieved high alignment with ISSB sustainability disclosure standards. Seventeen jurisdictions made the list. Bangladesh was one of them. The company it keeps: Australia, Brazil, Chile, Malaysia, Ghana, Kenya, Nigeria, and nine others.

This is not a certificate of achievement. It is an international expectation, and it carries real capital market consequences. When the IFRS Foundation formally profiles a jurisdiction, it signals to global investors, development finance institutions, correspondent banks, and ESG rating agencies that they should be measuring that jurisdiction’s financial institutions against ISSB standards. The profile raises the bar. Institutions that cannot clear it face visible, quantifiable consequences.

Bangladesh Bank established its IFRS S1 and S2 adoption roadmap in December 2023. The phased timeline is precise: limited intermediate reporting in 2024; limited disclosures in annual reports in 2025; more detailed disclosures in 2026; full disclosure required in 2027. The 2026 phase is the current financial year. Banks are expected to produce substantially more detailed and structured sustainability information now.

Bangladesh needs $980M per year to reach its 2030 renewable target. Green capital does not flow to institutions that cannot prove their sustainability credentials in internationally recognised formats.

The stakes are not abstract. Bangladesh’s renewable energy transition, its climate adaptation infrastructure, its green bond market development, its access to IFC and ADB sustainability-linked lending all of these depend on a banking sector that can produce credible, standardised, externally verifiable sustainability data. The ISSB framework is what ‘credible and standardised’ means in 2026.

The comparison with Pakistan is instructive. Pakistan adopted mandatory ISSB reporting for large listed companies from July 2025. Bangladesh has the mandate from its central bank. But implementation capacity the number of trained professionals who understand what IFRS S1 and S2 require, how to build the data systems, how to conduct materiality assessments, how to calculate Scope 1, 2, and 3 emissions lags behind the regulatory ambition.

Bangladesh’s 16 listed companies currently in the Bloomberg ESG universe including Grameenphone, BRAC Bank, Square Pharmaceuticals, Walton Hi-Tech, and others are being scored and ranked against global peers. As rating methodologies tighten around ISSB alignment, companies that cannot produce compliant disclosures will see their ESG scores decline. Lower scores mean higher cost of capital, reduced foreign institutional investor interest, and eventual exclusion from ESG-indexed funds.

Certified training in IFRS S1 and S2 reporting, materiality assessment, climate risk scenario analysis, and sustainability assurance — these are not optional skills for Bangladesh’s financial sector. They are the entry requirements for the international green capital market.