The Business of Fashion calls it fashion’s climate reckoning. The Daily Star calls it the renewables gambit. ESG Institute Bangladesh calls it a policy contradiction that is costing Bangladesh the trade access it cannot afford to lose.

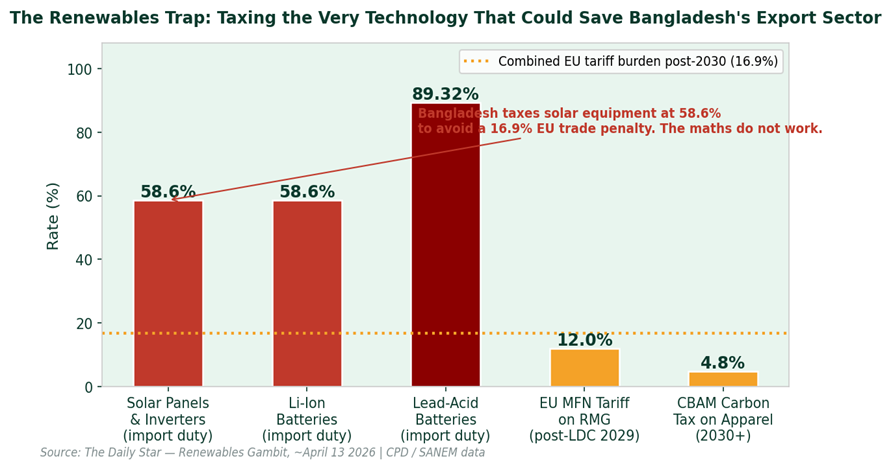

Here is the contradiction: Bangladesh’s garment sector exports to the EU face a compounding tariff threat. After LDC graduation in November 2026, the current Everything But Arms zero-duty arrangement transitions to a three-year grace period ending in 2029. After that, without GSP+ qualification, Bangladesh faces EU MFN tariffs of approximately 12% on garments. The EU’s Carbon Border Adjustment Mechanism CBAM is expected to expand to apparel by 2030, adding a carbon-linked charge on top. CPD calculates the CBAM exposure at 4.8%. Combined: 16.9% tariff burden from zero today.

The only way to reduce CBAM exposure is to decarbonise production. The most accessible decarbonisation pathway for garment factories is rooftop solar reducing grid electricity consumption and lowering Scope 2 emissions. And the import duty on solar panels, inverters, and mounting structures in Bangladesh is 58.6%. Lithium-ion batteries that make solar viable through load-shedding face the same 58.6% rate. Lead-acid batteries carry 89.32%.

Bangladesh solar equipment import duties vs incoming EU trade penalties, the country is taxing the very technology needed to avoid the carbon tariff. The combined post-2030 EU burden reaches 16.9% on garment exports

SANEM: Bangladesh risks losing 30% of EU garment exports if decarbonisation targets are not met by 2030. The 2030 deadline is four product cycles away.

Some factories are moving anyway, at significant cost and difficulty. Ha-Meem Group, one of Bangladesh’s largest RMG exporters, has installed 12 megawatts of rooftop solar capacity specifically targeting continued EU buyer orders after 2030. Managing Director AK Azad is direct about the motivation: during the Middle East energy crisis disrupting gas and fuel supply, the solar backup meant Ha-Meem continued operating when competitors with full grid dependency faced production shutdowns.

Global buyers are not waiting for policy clarity either. American Eagle now requires that at least 10% of electricity used by tier-one and tier-two suppliers comes from renewable sources. Levi Strauss and GAP have pledged to cut supply chain emissions by 42% by 2030. BGMEA has acknowledged that its manufacturers ‘are already operating on very tight margins, and any increase in utility costs directly affects competitiveness.’ The solar import duty makes those margins tighter while removing the one tool factories have to avoid the CBAM penalty.

The ask from the industry is clear: zero import duty on solar components used in export-oriented manufacturing. This is not a subsidy request. It is the removal of a self-defeating barrier. The revenue Bangladesh collects from solar equipment import duties is negligible compared to the export earnings at risk from CBAM-driven order losses.

The ‘E’ in ESG demands that we measure the carbon footprint of production and reduce it. The ‘G’ demands that government policy supports rather than obstructs that reduction. Removing the solar import duty is governance in action. Until it happens, Bangladesh’s factories face a choice between an expensive green transition and an even more expensive trade penalty. That is not a choice, it is a trap. And the EU’s 2030 deadline will not wait for the policy to catch up.