Pakistan is not a country that typically comes to mind when discussing renewable energy success stories. And yet, in 2025, it deployed 34,000 MW of distributed solar capacity — enough to cut its LNG demand by 15.4% in a single year. It did this without Bangladesh’s solar irradiance advantage, without Bangladesh’s garment export incentive, and without a comparable climate vulnerability argument.

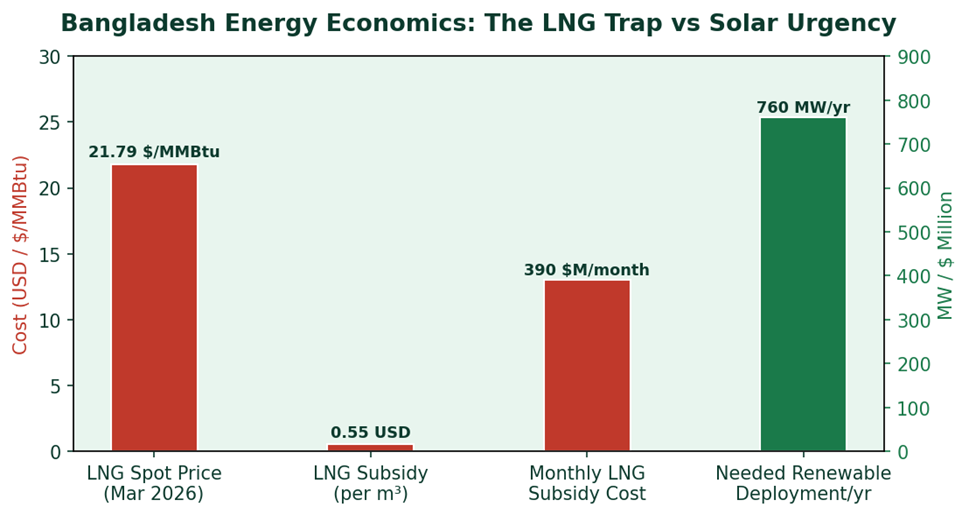

Bangladesh, meanwhile, is paying subsidies of Tk 67.5 per cubic metre on every unit of LNG it burns — at March 2026 spot prices of $21.79 per million British thermal units. The monthly subsidy bill for LNG alone exceeds $390 million. The Bangladesh Power Development Board is sitting on Tk 270 billion in unpaid invoices to independent power producers. The government is seeking a $2 billion emergency loan — which, at current burn rates, covers less than three months of combined diesel and LNG subsidies.

This is not an energy crisis. It is an energy policy crisis. And it has direct ESG consequences.

Bangladesh LNG cost trap: spot prices, subsidies, and the renewable deployment rate needed to escape it

On the environmental side: Bangladesh’s grid remains over 94% fossil-fuel dependent. Every factory, every bank branch, every hospital running on that grid has a carbon footprint it cannot honestly green up through any amount of internal efficiency. Scope 2 emissions — the emissions from purchased electricity — are built into Bangladesh’s industrial economy by default.

On the governance side: the fiscal bleeding from fossil fuel subsidies is crowding out investment in health, education, climate adaptation, and — yes — renewable energy infrastructure itself. It is a self-reinforcing trap.

The path out is not complicated. Bangladesh needs to deploy approximately 760 MW of renewable energy per year between 2026 and 2030 to reach its 20% clean energy target. That is achievable. The Bangladesh Economic Zones Authority has already signed an advisory agreement with the Asian Development Bank for a 100–200 MW utility-scale solar project. Pran-RFL and IFC are planning a dedicated solar plant for H&M’s supplier factories. Robi Telecom is moving toward a 100 MW solar project.

These are green shoots — but they are not a green grid. The gap between current renewable capacity (1,690 MW) and the 2030 target (5,851 MW) remains nearly 4,000 MW.

What Bangladesh needs now is not more feasibility studies. It needs the Merchant Power Policy framework that was recently approved to actually unlock corporate power purchase agreements at scale. It needs import duty exemptions on solar panels and battery storage — not just inverters. It needs SREDA to run technician training programmes that can match deployment speed.

For the private sector, the calculus is increasingly simple: every taka spent on diesel generators and unsubsidised grid power is a taka not spent on market-competitive production. Companies that move to solar — rooftop, dedicated plant, or off-take agreement — lock in energy cost certainty for a decade. That is an ESG gain and a financial gain simultaneously.

Pakistan proved it can be done fast, at scale, without perfect conditions. Bangladesh has better sun, a more urgent fiscal situation, and a $17.5 billion trade cliff to negotiate.

The subsidy meter is running. The solar potential is sitting untapped. The choice is not between fossil fuels and renewables anymore. The choice is between subsidised dependency and competitive independence.

Which side of that choice is your organization on?