If Bangladesh were a listed company, and the SDGs were its annual performance report, analysts would be writing sell notes.

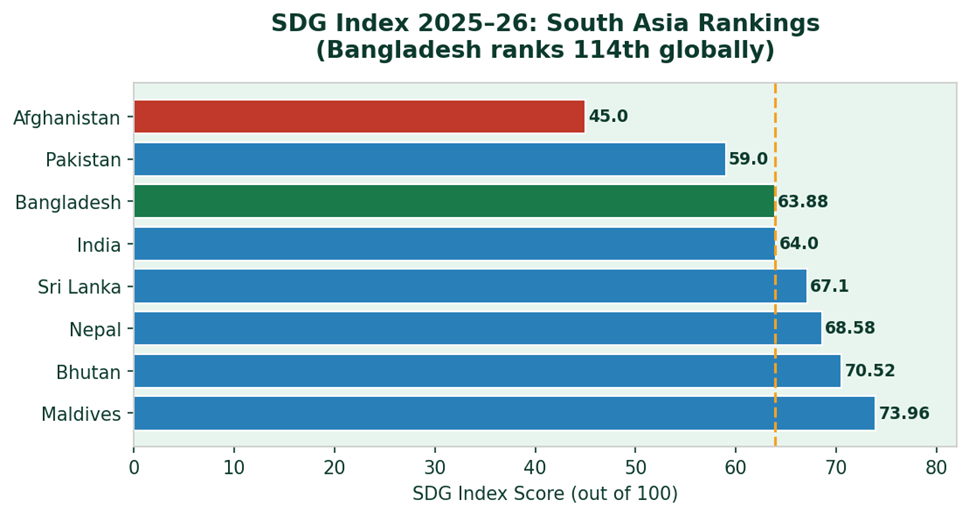

As of March 28, 2026, Bangladesh ranks 114th out of 167 countries globally on the SDG Index, scoring 63.88 out of 100. In South Asia, it sits ahead of only Pakistan and Afghanistan. The Maldives — a small island nation — outscores Bangladesh by 10 full points. Nepal and Bhutan, often overlooked in regional comparisons, are also ahead.

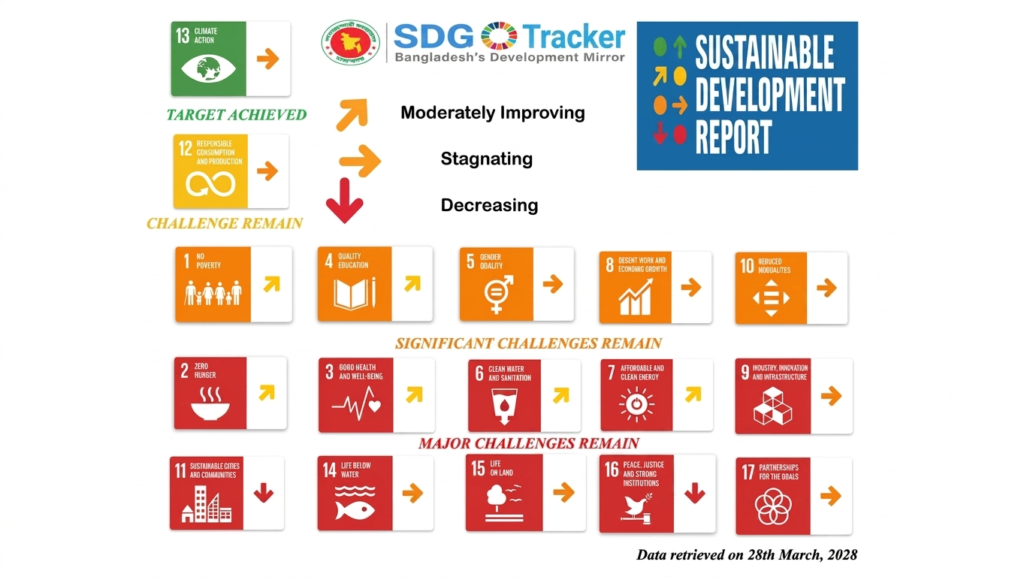

More alarming than the ranking is the direction of travel. Only 20.8% of Bangladesh’s SDG targets are on track. A further 44.2% show limited progress, and 35.1% are actively worsening.

Let that last figure sit for a moment. More than a third of Bangladesh’s sustainable development targets are moving in the wrong direction.

SDG Index 2025–26: South Asian rankings — Bangladesh sits near the bottom at 63.88/100

The areas of regression are not abstract. SDG 13 — climate action — is declining, even as Bangladesh remains the 9th most climate-exposed country on the planet. The nation’s CO₂ emissions from fossil fuels and cement production continue to rise. SDG 11 — sustainable cities — is deteriorating as Dhaka’s infrastructure fails to keep pace with urban migration. SDG 12 — responsible consumption — is stalled, with mounting plastic pollution and weak waste management systems.

For the ESG community, this data has a very specific implication: Bangladesh cannot credibly claim to be a sustainable investment destination while its own sustainability metrics are falling. Foreign investors, buyers, and development finance institutions increasingly use SDG performance as a proxy for country-level ESG risk. A country at 114th and declining is flagged — not funded.

The SDGs are not a separate agenda from ESG. They are the macro-framework within which corporate ESG sits. A company in Bangladesh can publish a beautiful sustainability report, but if the national grid is fossil-fuel dependent, the city is unliveable, and the climate risk is rising unchecked, that report has a credibility ceiling.

What is holding Bangladesh back? The SDG Transformation Center data points to three structural failures. First, institutional fragmentation: ministries working on SDGs in silos without coordination. Second, financing gaps: the country’s SDG financing gap is enormous, and domestic revenue mobilization remains weak. Third, data quality: significant data missing across key indicators makes monitoring and course correction nearly impossible.

The good news — and there is some — is that Bangladesh scores a striking 96.30 on the International Spillover Index, meaning its development does not cause harm to other countries’ SDG progress. That is a foundation to build on.

But building on a foundation requires acknowledging what the data says plainly: the current trajectory will not get Bangladesh to the SDGs by 2030. Not even close.

For businesses, this is both a warning and an opportunity. Companies that build genuine ESG practices — not greenwashing, not checkbox compliance, but measurable progress on emissions, labour rights, governance, and community impact — are positioning themselves ahead of where the country’s regulatory and investment environment is going.

The SDG trajectory will improve. The question is whether your business will be part of the improvement, or caught off-guard when the tide turns.

Bangladesh’s SDG score is 63.88 today. What is yours?