On 26 December 2023, Bangladesh Bank issued SFD Circular 06/2023 — a regulatory directive that fundamentally changed the disclosure obligations of every scheduled bank and finance company in Bangladesh.

The circular mandated the implementation of IFRS S1 and IFRS S2: the International Sustainability Standards Board’s standards for sustainability-related financial disclosure and climate-related disclosure respectively. Bangladesh became one of only 17 countries in the world to have a published, finalised ISSB jurisdictional profile — ahead of most of its South Asian peers, and ahead of many developed economies.

This was a significant regulatory moment. It positioned Bangladesh’s financial sector as part of the global baseline for sustainability disclosure. It created a legal obligation — not a guideline, not a recommendation — for banks to disclose sustainability risks and climate-related financial information alongside their standard financial statements.

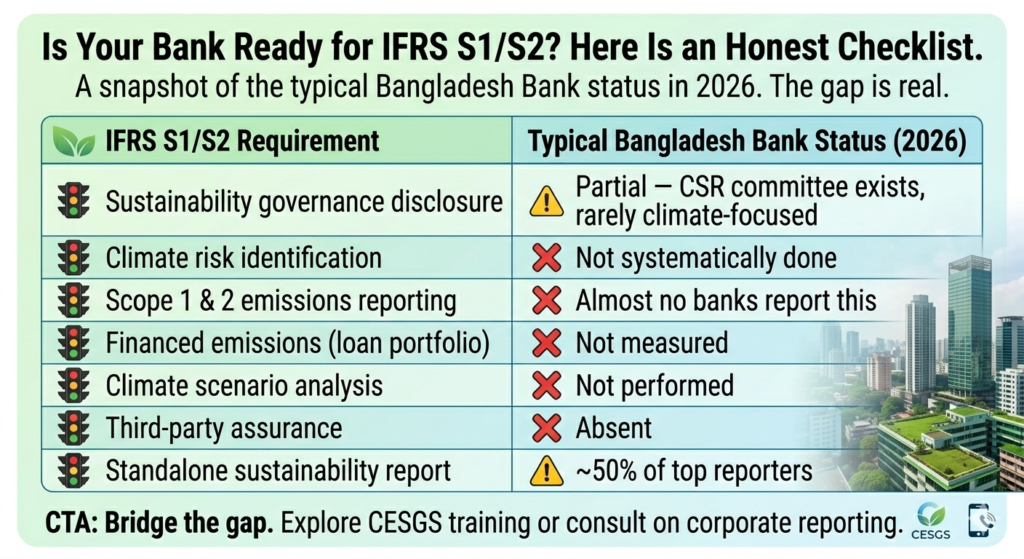

And yet, a survey by the Institute of Cost Accountants of Bangladesh found that among 25 companies known for their annual reporting excellence, only half had issued standalone sustainability reports. A mere third referenced recognised frameworks like GRI. None — zero — reported on the scope of their emissions or used assurance statements.

The regulation arrived. The capacity did not come with it.

Source: ICAB survey findings; Financial Express analysis, 2025

What IFRS S1 and S2 Actually Require

For those encountering these standards for the first time, it is worth being precise about what they ask of an organisation.

IFRS S1 sets out general requirements for disclosing sustainability-related financial information. It requires organisations to disclose all material information about sustainability-related risks and opportunities that could reasonably be expected to affect their financial performance and prospects. This means: identifying what sustainability issues matter to the business, explaining how governance oversees those issues, how strategy integrates them, and how the organisation measures progress.

IFRS S2 is specifically about climate. It requires disclosure of climate-related risks and opportunities — physical risks (flooding, heat stress, supply chain disruption from extreme weather) and transition risks (policy changes, technology shifts, market changes as the economy decarbonises). It requires Scope 1 and Scope 2 greenhouse gas emissions data, climate scenario analysis, and disclosure of how climate considerations are integrated into capital allocation decisions.

For a Bangladesh bank, this means: Can you say how much of your loan portfolio is exposed to climate risk? Do you know which industries in your book are most exposed to transition risk from the EU’s CBAM or carbon pricing policies? Can you report your own operational emissions? Do your risk committees discuss climate as a financial risk, not just an environmental one?

The honest answer in most Bangladeshi banks today is: no, we cannot. Not credibly. Not yet.

Why This Gap Matters Beyond Compliance

The temptation is to treat IFRS S1 and S2 as a compliance problem — something to manage with a new template and an updated annual report chapter. That would be a mistake, and not just for ethical reasons.

Financed emissions are becoming a credit risk signal. International banks and development finance institutions increasingly assess the carbon intensity of a bank’s loan portfolio when making correspondent banking decisions and setting terms for wholesale funding. A Bangladeshi bank that cannot report its financed emissions is increasingly opaque to the counterparties it needs for international operations.

Green and sustainable finance is the growth segment. Bangladesh Bank’s own data shows green financing grew from 4% of term loan disbursements in 2020 to 15.2% by late 2024. Sustainable financing grew from 8% to 39.2% in the same period. The institutions best placed to capture this growth are the ones that understand and can report on sustainability performance — not the ones scrambling to retroactively understand what IFRS S2 requires.

| Year | Green Finance (% of term loans) | Sustainable Finance (% of total) |

|---|---|---|

| 2020 | 4.0% | 8.0% |

| 2021 | 6.5% | 12.0% |

| 2022 | 9.0% | 22.0% |

| 2023 | 12.0% | 31.0% |

| Sep 2024 | 15.2% | 39.2% |

Chart: Bangladesh Sustainable & Green Finance Growth. Source: FICCI / Bangladesh Bank data, 2025

IFRS S1/S2 literacy is becoming a hiring criterion. International financial institutions operating in Bangladesh, DFIs providing project finance, and local banks with international ambitions are increasingly looking for professionals who can work with sustainability disclosure frameworks. This is a skills market in formation — and the professionals who build that capability now will have significant career advantage within five years.

The Phased Reality and What It Means

Bangladesh Bank has proposed a phased implementation approach, with full compliance scaled toward 2027. This is pragmatic — the standards are genuinely demanding, and organisations need time to build data systems, train staff, and develop governance processes.

But phased does not mean optional, and 2027 is not far away. Organisations that begin now have three years to build methodically. Organisations that begin in 2026 have one year to scramble. And organisations that wait until a regulatory enforcement action prompts action will find that the reputational and operational cost of starting late is higher than the cost of starting now.

The Financial Express noted what is perhaps the sharpest summary of Bangladesh’s preparedness challenge: awareness of IFRS S1 and S2 among financial institution owners and managers remains low, and capacity limitations — infrastructure, technical expertise, financial resources — are concentrated among exactly the organisations that most need to comply.

The Opportunity Hidden Inside the Challenge

Bangladesh’s IFRS S1/S2 mandate is not just a compliance burden. It is an invitation to become a regional leader in sustainable finance — which is the highest-growth segment of financial services globally.

The banks that build genuine IFRS S2-aligned climate risk frameworks will be better positioned for Asian Development Bank and IFC funding. They will attract institutional investors whose mandates require ISSB-aligned reporting from counterparties. They will be able to offer credible green and sustainability-linked loan products rather than relabelling existing products with green packaging.

But all of that starts with one thing: trained professionals who actually understand what the standards require and how to implement them.

ESG Institute Bangladesh is Bangladesh’s only dedicated ESG education and advisory institute. We offer professional certification, corporate training, and sustainability reporting advisory built specifically for the Bangladesh context. The ESG Excellence Awards Bangladesh 2026 recognise organisations already building this future. Applications open now.

Professional Trainings (Diploma, Accreditations, In-Depth Workshops): https://esginstitutebd.com/| Join the 2026 ESG Awards: esgawardsbd.com