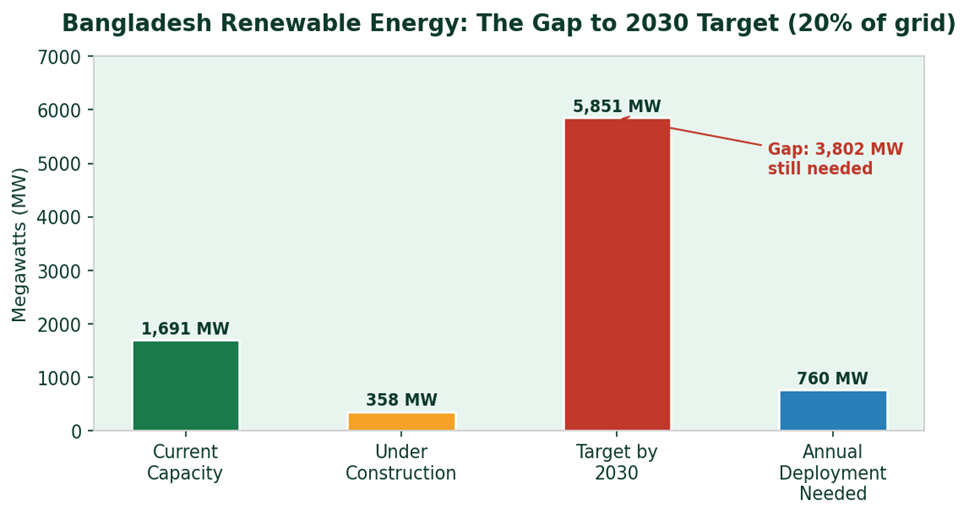

📊 Bangladesh’s renewable energy gap: current capacity vs the 2030 target requiring ~760 MW deployed per year

Bangladesh has pledged to generate 20% of its electricity from renewable sources by 2030. It currently generates around 5.4% from renewables. The target requires 5,851 MW of clean capacity. The country has 1,690 MW installed and another 358 MW under construction.

Do the maths. Bangladesh needs to deploy approximately 760 MW of new renewable capacity every single year for the next four years. In the last several years combined, it has fallen short of that annual figure.

This is not a technology problem. Solar is now the cheapest source of electricity in history. It is cheaper than coal, cheaper than gas, and dramatically cheaper than the LNG spot purchases Bangladesh is making to keep the lights on. The problem is policy, financing, and execution.

Start with policy. Until recently, Bangladesh lacked a functioning framework for corporate power purchase agreements — the mechanism that allows large companies to contract directly with renewable energy producers. The new Merchant Power Policy has created that framework. But the service-level agreements covering wheeling charges and dispute resolution still need to be finalised before projects can actually move.

Then there is land. Bangladesh is one of the most densely populated countries on earth. Utility-scale solar requires land that agriculture-dependent communities cannot easily spare. The solution — mapping available space within economic zones and rooftops — is known. The National Special Economic Zone has 5,980 acres of designated free space. That is space that could host hundreds of megawatts. The ADB has already signed an advisory agreement to develop a 100–200 MW project there. It needs to move faster.

Financing is the third constraint. International development finance — from ADB, IFC, the EU’s €381.5 million renewable energy facility, and the Green Climate Fund — is available and allocated. But disbursement mechanisms, government counterpart guarantees, and off-taker risk frameworks remain incomplete. Bangladesh’s credit rating fell to B2 in November 2024, which makes commercial borrowing for renewable infrastructure more expensive.

Innovative financing structures — green bonds, green sukuk, corporate off-take agreements — can de-risk projects for private capital. But they require a regulatory framework that treats renewable energy investment as a priority, not an afterthought.

For the ESG community, the renewable energy gap is not just an environmental issue. It is a supply chain issue. The EU’s Carbon Border Adjustment Mechanism is set to expand to apparel by 2030. Factories running on diesel generators or coal-heavy grid power will face a carbon tax on top of the tariffs they already pay. BGMEA has committed to sourcing 30% renewable energy. Getting there requires a functioning renewable energy market — which requires the policy and financing fixes described above.

There is reason for optimism. Pran-RFL, supported by IFC, is building a dedicated solar plant for H&M’s supplier network. Robi Telecom is developing a 100 MW solar project. These are private sector actors moving ahead of the grid. They are proving the model.

What Bangladesh needs now is for those models to be replicated at industrial scale — thousands of rooftop installations, dozens of solar zone projects, and a government that treats every day of fossil fuel dependence as a cost it cannot afford.

760 MW per year. That is the number. Build it, or pay for it in tariffs, subsidies, and lost market access.

The choice has already been made for us by the physics of climate change and the economics of global trade. The only remaining question is speed.