January 1, 2026. That is the date the European Union’s Carbon Border Adjustment Mechanism moved from a reporting phase into enforcement. Importers of covered goods now must register as authorised declarants and purchase carbon certificates based on the emissions embedded in their products. The first surrender of those certificates — for 2026 imports — is due by September 30, 2027.

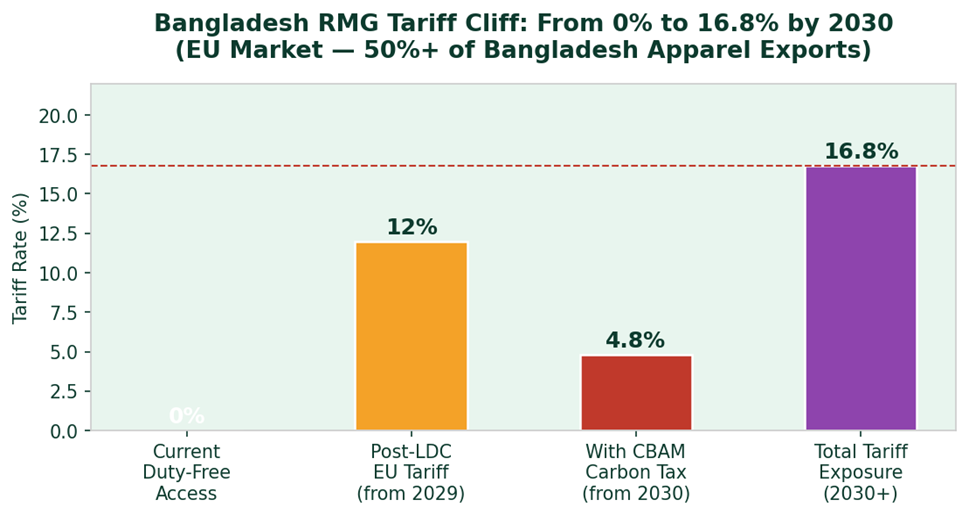

Bangladesh RMG tariff trajectory: from duty-free access today to a potential 16.8% combined burden by 2030

Right now, apparel is not on the CBAM product list. But the EU’s stated plan is to include all imported goods by 2030. Given that apparel accounts for over 80% of Bangladesh’s total exports and the EU buys more than half of those garments, the expansion of CBAM to textiles is the single most consequential regulatory development in Bangladesh’s trade history.

The numbers from a recent Centre for Policy Dialogue study are precise: if current emission levels in Bangladesh’s garment sector persist, an additional 4.8% carbon tax will be imposed after 2030. Add that to the 12% average EU tariff that kicks in after Bangladesh loses its duty-free LDC access in 2029, and you arrive at a combined tariff burden of approximately 16.8%.

That is a tariff cliff. From 0% today to 16.8% in four years, for the same products, to the same buyers, from the same factories.

Bangladesh’s RMG sector currently has only 5.38% renewable energy capacity in its electricity generation mix. Competitors like India, Cambodia, and Pakistan have moved significantly faster on greening their industrial energy systems. If orders shift to lower-carbon producers — which buyers under CBAM pressure will have financial incentives to do — Bangladesh does not just lose market share. It loses the jobs, the foreign exchange earnings, and the development trajectory that the entire economy depends on.

The South Asian Network on Economic Modeling estimates a possible 30% decline in Bangladesh’s EU apparel exports if the decarbonisation gap is not closed.

BGMEA President Mahmud Hasan Khan Babu has said factories are already working toward 30% renewable energy in line with EU requirements, and that nearly 300 factories hold LEED certification from the US Green Building Council. That is real progress. But LEED certification addresses building design, not grid-sourced electricity emissions. The CBAM will measure actual embedded carbon — the emissions from energy used in production — not the energy efficiency of a factory’s structural design.

This distinction matters enormously. A factory can be LEED Platinum and still carry significant Scope 2 carbon emissions if it runs on grid power generated by gas and oil. The EU’s carbon certificate system will price that gap.

CPD’s policy recommendations are clear: invest in clean energy, develop a domestic carbon pricing mechanism, engage with the WTO to ensure CBAM is not used as a protectionist tool, and build CBAM monitoring capacity at the sector and factory level.

For ESG practitioners, this is a moment of maximum urgency. The companies that begin measuring, reporting, and reducing their embedded carbon now will have a quantified advantage over those that wait. Buyers negotiating 2028 and 2029 order books will be factoring carbon costs into sourcing decisions before CBAM even applies to apparel.

The EU’s carbon wall is being built. Bangladesh did not design it, did not vote for it, and has legitimate grievances about trade fairness. But the wall is going up regardless.

The question is not whether to prepare. The question is whether to start today or spend the next four years hoping the wall stays on the other side of someone else’s supply chain.

It will not.