On the evening of April 16, 2026, Bangladesh’s Cabinet Secretary made an announcement that turned heads across the country’s energy and ESG communities: the new government of Prime Minister Tarique Rahman had decided to develop 10,000 megawatts of solar power on state-owned public land by 2030, opening it to private entrepreneurs under a public-private partnership model. Tariff targets: between Tk 4 and Tk 8 per unit. A committee has been formed. Implementation was expected to begin within days.

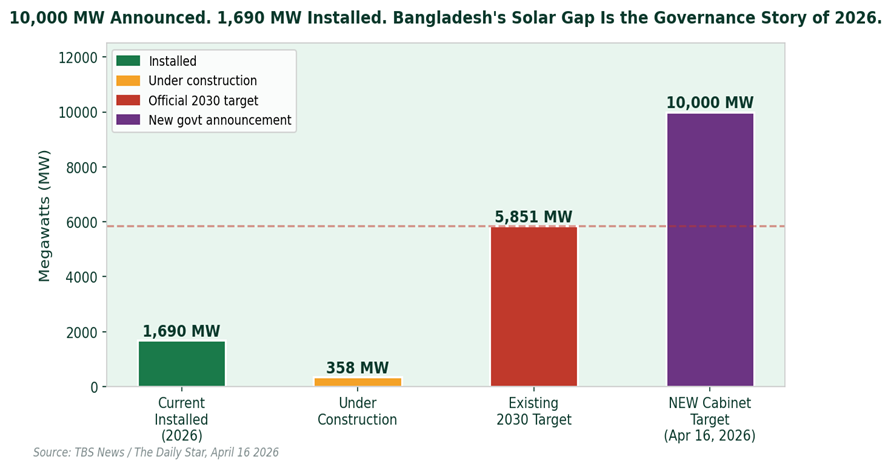

Let’s put the number in context. Bangladesh currently has 1,690 MW of installed renewable capacity. There are 358 MW under construction. The existing official 2030 target set under the Renewable Energy Policy 2025 was 5,851 MW. The new announcement nearly doubles that. It is the most ambitious renewable energy target this country has set. It is also being set by a government that inherited a power sector with zero utility-scale renewable projects added to the pipeline between August 2024 and December 2025.

Bangladesh renewable energy: installed capacity vs pipeline vs 2030 target vs new April 16 cabinet announcement — the ambition gap tells the governance story

“Earlier solar initiatives did not perform as expected.” Cabinet Secretary Nasimul Ghani, April 16 2026

That acknowledgement matters. Bangladesh has missed every renewable energy target it has set since 2008. The 10% target for 2020 was not met. The 3,000 MW rooftop solar programme announced in July 2025 could not scale. The previous government cancelled 33–34 mature renewable projects worth an estimated 1,300 MW. Investor confidence has been damaged by policy reversals, missing implementation agreements, and financing gaps.

The April 16 announcement addresses the land constraint which has been cited as a barrier for years by directing authorities to identify unused government land near hospitals, educational institutions, and public offices for solar development. This is the right move. Bangladesh has far more suitable land than commonly assumed. The IEEFA and multiple studies confirm this.

But land alone does not build a solar park. What investors need is the full governance architecture: transparent procurement processes with clear timelines, implementation agreements that make projects bankable for lenders, competitive wheeling charges under the Merchant Power Policy framework, and independent monitoring of delivery. None of these have been confirmed yet.

This announcement is both welcome and a governance accountability test. The ‘G’ in ESG is ultimately about whether institutions deliver on what they commit to. Bangladesh’s solar ambition is real. Its delivery track record is not. International green capital the billions of dollars Bangladesh needs to finance this transition — will follow implementation, not announcements. Quarterly progress reports, disclosed tender outcomes, and verified installation milestones are the currency of credibility.

The government has 1,346 days until December 31, 2030. 10,000 MW in 1,346 days is 7.4 MW per day. Bangladesh has never come close to that rate. But it has never had this level of political commitment, this level of global market pressure, and this level of available solar technology at this price point either. The conditions for success are real. The question is governance.