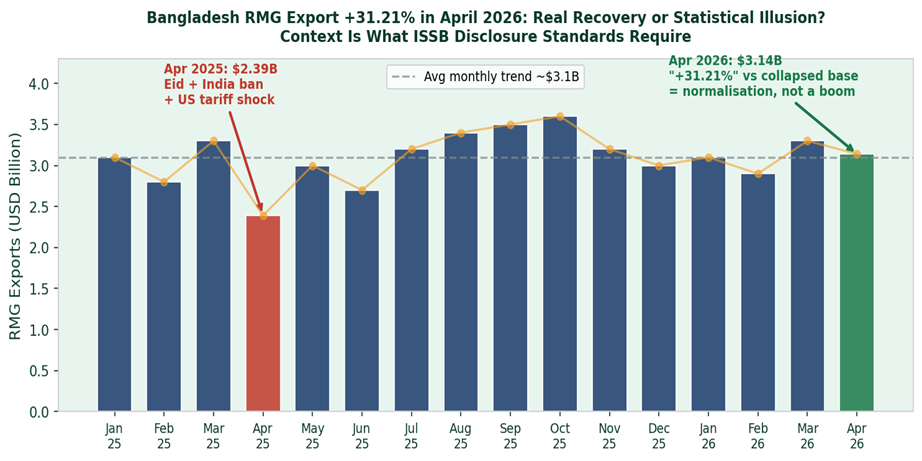

Bangladesh’s Export Promotion Bureau data published in early May 2026 shows RMG exports of $3.14 billion in April 2026 — a 31.21% year-on-year increase. Knitwear exports rose 30.02%. Woven garments climbed 32.65%. The numbers were reported prominently and met with celebration across industry and government communications.

The number is real. The framing deserves scrutiny.

Month-by-month Bangladesh RMG exports showing April 2025’s artificial collapse and April 2026’s return to normal — the 31% “growth” is normalisation against a depressed base, not a new peak

April 2025 was an anomalous month by any industry measure. Three separate events compressed performance well below the sector’s running rate simultaneously. First: Eid-ul-Fitr fell in late March 2025, with the extended holiday running into April, reducing factory working days and delaying shipments across the board. Second: India revoked Bangladesh’s transshipment facility on April 8, 2025, disrupting an established logistics route and creating immediate shipment backlogs. Third: initial USTR Section 301 investigation announcements in March 2025 generated buyer uncertainty, with some orders paused during April. The result was an April 2025 export figure of $2.39 billion — significantly below the sector’s typical monthly range of $3.0–3.4 billion.

Industry insiders are explicit: April 2026 is normalisation, not a new high. Reporting it as 31% growth without this context is selective disclosure — exactly what ISSB standards are designed to prevent.

A 31.21% recovery from an artificially depressed base is not 31.21% organic growth. Industry insiders cited by Textile Focus are explicit: this represents normalisation, not exceptional performance. Reporting the headline figure without the base-effect context creates a materially misleading impression.

This matters beyond Bangladesh’s export statistics. It is a real-time demonstration of the core principle of ISSB sustainability disclosure standards: material context must accompany performance data. IFRS S1 requires that sustainability-related information — and all material metrics — be presented in a way that is complete, comparable, and free from material misstatement. Removing the asterisk is not transparency. It is selective reporting. The April 2026 export number is a perfect teaching case. Every sustainability metric your organisation reports deserves the same rigour: the number and its context are inseparable.