In June 2025, the IFRS Foundation published something unprecedented: formal jurisdictional profiles for countries with high alignment to ISSB sustainability disclosure standards. Only 17 jurisdictions made this initial list. Bangladesh was one of them — alongside Australia, Brazil, Chile, Malaysia, Ghana, Kenya, and Nigeria.

ISSB stands for the International Sustainability Standards Board. It publishes IFRS S1, which requires companies to disclose sustainability-related risks and opportunities, and IFRS S2, which covers climate-specific disclosures including greenhouse gas emissions, climate-related risks, and scenario analysis. Together, these two standards are becoming the global baseline for corporate sustainability reporting, the ESG equivalent of what IFRS accounting standards did for financial reporting over the past three decades.

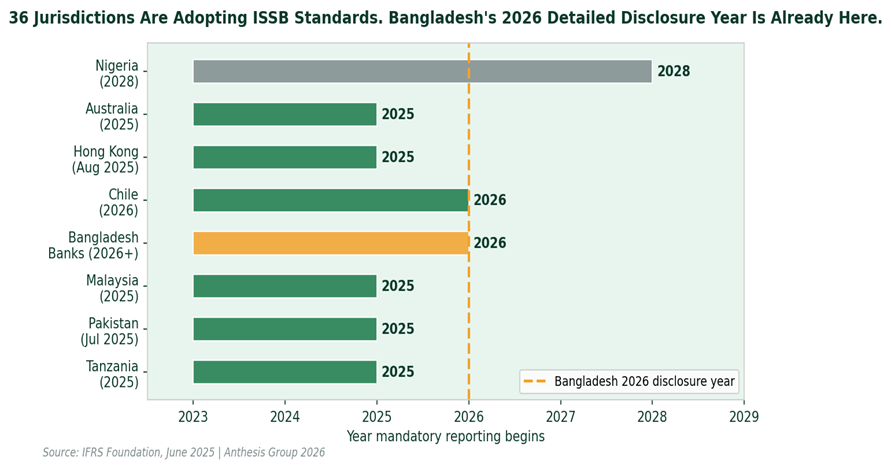

ISSB mandatory adoption timelines across key jurisdictions — Bangladesh’s 2026 “more detailed disclosures” year sits in the middle of a global wave already underway

As of mid-2026, 36 jurisdictions have adopted, formally begun adopting, or are actively integrating ISSB standards into their regulatory frameworks. These jurisdictions represent more than 55% of global GDP and the overwhelming majority of global capital markets. What this means practically: international investors, lenders, and rating agencies are building their ESG analysis around ISSB-aligned data. Institutions that cannot produce it are increasingly invisible to international capital.

Pakistan made ISSB mandatory for large listed companies from July 2025. Bangladesh has the mandate. The gap is implementation capacity.

Bangladesh Bank issued its IFRS S1 and S2 adoption guidelines in December 2023, establishing a clear phased roadmap: limited reporting in 2024, disclosures in annual reports in 2025, more detailed disclosures in 2026, and full disclosure in 2027. The 2026 phase is active now. Banks are required to produce substantially more detailed sustainability information in their current financial year reporting.

Why does this connect to real money? Bangladesh needs approximately $980 million annually to meet its 2030 renewable energy target. A significant portion of this must come from international green finance — development bank lending, green bonds, ESG-linked facilities, and concessional climate funds. These instruments are designed for institutions that can prove their sustainability credentials in standardised, comparable, internationally recognised formats. ISSB is that format.

The implementation gap is honest and significant. Knowing that IFRS S1 and S2 exist and being able to produce compliant disclosures are vastly different things. Data collection systems, materiality assessments, climate risk scenario analysis, Scope 1, 2, and 3 emissions calculations, these require trained professionals, upgraded reporting infrastructure, and independent assurance processes.

ESG Institute Bangladesh trains professionals specifically for this transition. The 2026 disclosure year is not waiting for capacity to catch up. Every bank, every listed company, every institution seeking international green capital needs people who understand what ISSB requires, how to collect the data, and how to present it credibly. That expertise is what ESG Institute Bangladesh provides.