There is a sentence buried in most global fashion brand sustainability reports that Bangladesh’s garment factory owners should read very carefully: ‘We are committed to achieving net-zero emissions across our supply chain by 2030.’

Thousands of factory owners have been thinking that the green transition in global fashion is being financed on the backs of the suppliers who can least afford it.

Your factory is that supply chain. The net-zero target is now your problem. The bill, in most cases, is yours too.

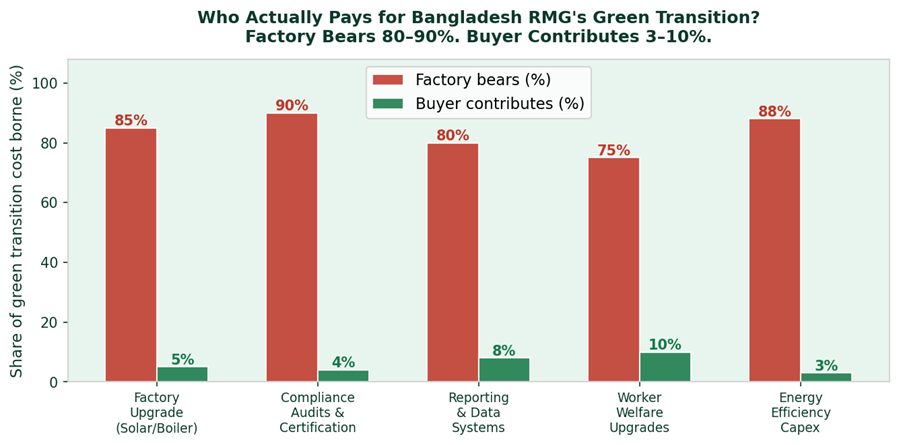

Who actually pays for Bangladesh RMG’s green transition, factories carry 80–90% of the cost, buyers contribute 3–10%.

The argument is specific and the numbers are real. Installing rooftop solar for a mid-sized factory costs Tk 2–3 crore upfront. Upgrading to an energy-efficient boiler system: Tk 50–80 lakh. Commissioning a full carbon footprint audit and setting up an emissions reporting system: Tk 15–25 lakh. Combined, this is more capital than most of Bangladesh’s SME factory owners can access in the current credit environment where private sector credit growth has fallen to 6.1% and bank lending to manufacturing is constrained by elevated NPLs.

“A truly sustainable global supply chain cannot be achieved if costs, risks, and responsibilities are distributed unfairly.” — Mostafiz Uddin, The Daily Star, April 21 2026

Meanwhile, the brands issuing these compliance requirements have direct access to the fastest-growing pool of cheap capital in global finance: green bonds, sustainability-linked loans, ESG-indexed equity, development finance institution co-investment, and blended finance facilities specifically designed for supply chain decarbonisation. H&M, Inditex, and Primark each have sustainability-linked financing arrangements worth hundreds of millions of euros. The price adjustment passed to Bangladeshi suppliers for going green: close to zero.

We are not arguing against decarbonisation. We are arguing against the current distribution of who finances it. The buyers who benefit commercially from cheap, compliant supply chains should contribute to the cost of making those supply chains compliant. If a brand sources 50 million pieces from Bangladesh annually, adding $0.02 per piece generates $1 million, enough to fund solar installations for 30–40 SME factories. That calculation is not complicated. It has simply not been made a requirement.

What happens instead is a market selection effect that Bangladesh should be alarmed about: large, well-capitalised factories — DBL Group, Ha-Meem, Beximco — can absorb green compliance costs and retain premium buyer relationships. The thousands of SME factories that built Bangladesh into a $39 billion export economy cannot. They get dropped. They close. The 400 factory closures Bangladesh has recorded in the past three years are not random. They are concentrated precisely among the factories least able to fund the compliance requirements buyers now demand. Buyer accountability is not charity. It is supply chain governance the ‘G’ in ESG applied at the commercial relationship level. The EU’s Corporate Sustainability Due Diligence Directive, effective 2029, will legally require brands to assess and address adverse impacts across their supply chains. That legal framework should include financing obligations, not just audit obligations. Bangladesh’s government, BGMEA, and trade negotiators should make this explicit in every bilateral discussion with EU and UK counterparts. The green transition is necessary. Who funds it is a governance question and Bangladesh deserves a better answer than ‘you do.’