Bangladesh’s capital market ESG landscape is approaching a regulatory inflection point. The Bangladesh Securities and Exchange Commission is actively revising its Corporate Governance Code to incorporate ESG reporting as a binding legal requirement — not a voluntary recommendation. Simultaneously, the Financial Reporting Council is adopting IFRS S1 and S2, the ISSB standards for general sustainability and climate-related disclosures, as the framework for listed company sustainability reporting.

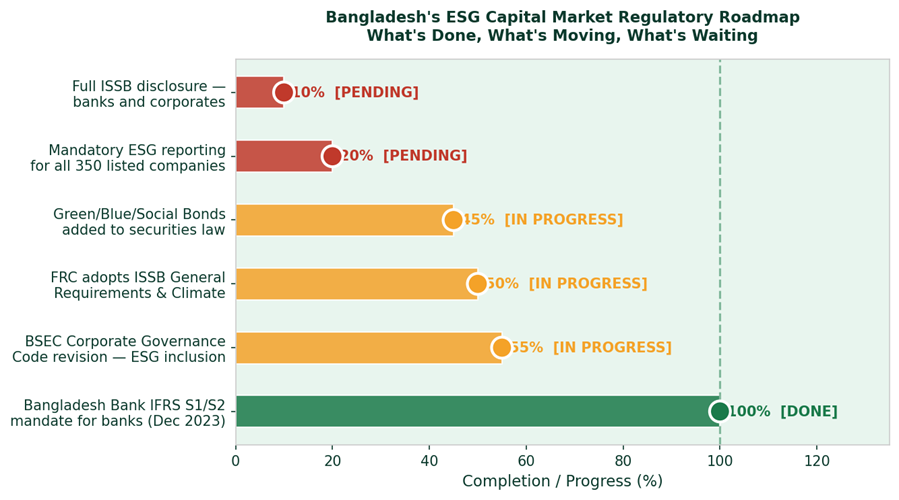

Bangladesh ESG capital market regulatory progress, colour-coded by status: green (complete), amber (in progress), red (pending). The roadmap is moving faster than market capacity to comply.

These are decisions in active motion. On April 16, 2026, the PM’s special assistant Tanvir Ghani visited BSEC specifically to review capital market reform progress. ESG integration into the corporate governance framework was confirmed as part of the agenda. The regulatory direction is set. The timeline is the remaining open question.

The current baseline makes the challenge sharply visible. Of 350 companies listed on the Dhaka Stock Exchange, only 16 appear in the Bloomberg ESG universe, the international database institutional investors use for portfolio construction. That means 334 listed companies are invisible to the fastest-growing segment of global capital markets. No ESG rating. No standardized disclosures. No presence in ESG-screened investment indices.

When the mandatory code arrives, 334 companies face an immediate compliance gap. The training that prevents that gap needs to start now, before the regulation, not after it.

When mandatory ESG reporting arrives and it clearly is these 334 companies will face compliance requirements with no preparation, no trained personnel, and no established systems. ESG reporting requires capabilities that do not yet exist at scale in Bangladesh’s corporate sector: materiality assessment, stakeholder mapping, Scope 1/2/3 emissions calculation, climate risk scenario analysis, and independent assurance. These are not extensions of accounting practice. They are a different discipline.

Bangladesh Bank’s 2023 IFRS S1/S2 mandate for the banking sector was the starting signal. BSEC’s corporate governance revision extends this requirement across the capital market. FRC adoption of ISSB frameworks aligns Bangladesh with 36+ jurisdictions globally representing 55%+ of world GDP where ISSB-aligned reporting is already mandatory or in progress. The regulatory reform is being written now. The professionals who will make compliance possible need to be trained now.